Nine mobile network operators across 48 countries in Africa and the Middle East have joined forces on the GSM Association’s Mobile Money Interoperability (MMI) program. The program aims to develop standards and implement convenient and affordable financial services across the regions, where many citizens have limited access to traditional banking services.

Mobile money transactions in Sub-Saharan Africa and the Middle East totaled US$5.7 billion last year, and more than a quarter of Kenya’s economy now flows through groundbreaking service M-Pesa – which has been adopted by 56 percent of Kenyans since its introduction by Vodafone and Safaricom in 2007 – without touching a bank account.

But while Kenya stands as an exemplar of mobile money, far ahead of even the US in usage of payments through a mobile phone, other countries have been much slower to adopt the model – thanks in part to regulatory challenges that hold back innovation. There’s hope that this MMI program will accelerate growth through collaborative development of best practice guidelines, regulatory support, performance benchmarks, and interoperability between services.

It could have widespread implications, as an estimated 1.7 billion people in lower to middle income countries own a mobile phone (primarily with prepaid credit), yet currently lack access to the financial services taken for granted in the developed world. Mobile money is now available in most developing markets, although the 2013 GSMA Mobile Money for the Unbanked State of the Industry report indicates that services tend to be limited outside of East Africa.

That’s where MMI comes in. The initiative is meant to connect mobile network operators with banks, governments, and other partners in a bid to allow access to more mobile financial services for a broader range of people. This would provide a means for them to take out insurance, invest in savings accounts, make and accept payments, and send money across borders.

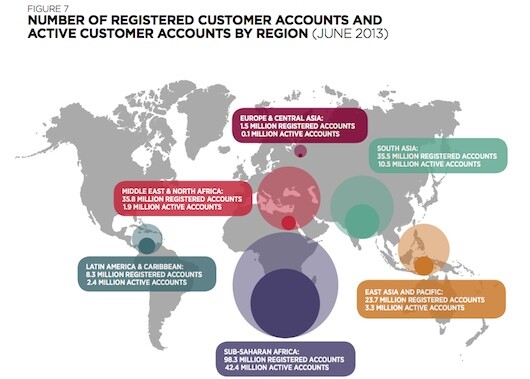

Explosive growth in the field has seen mobile money accounts outnumber bank accounts in nine African markets, with 98 million registered and over 60 million active in Sub-Saharan Africa as of June 2013. Competition is also growing – 52 countries (36 of which are in Sub-Saharan Africa) have at least two mobile money services, and 27 of those have three or more. This could lead to accelerated innovation, but without interoperability it will devolve into a total mess.

Most existing mobile money services act as closed-loop systems wherein electronic money must be converted to cash before it can be sent to someone on another mobile money service. But cooperation within and across regions should soon see these kinds of barriers disappear in favor of interconnected schemes that seamlessly (no doubt with some transaction fees) transfer funds from one service to another at the press of a button.

"Mobile money is a young industry, with over 80 percent of all deployments launched during or after 2010," said GSMA Director General Anne Bouverot. It's a field under rapid, enthusiastic, unparalleled growth, and it falls now on the signees of the Mobile Money Interoperability program to steer the ship to safe waters as mobile money races toward ubiquity across all of Africa and the Middle East.

Source: GSMA